Refinancing: find out what your friends already know

You value the opinions of your family and friends, who want to help you get debt free. Get up to speed and understand the buzz on refinancing.

Home

Student Debt Counseling

Federal Student Loans

Ready, Get Set, Refinance

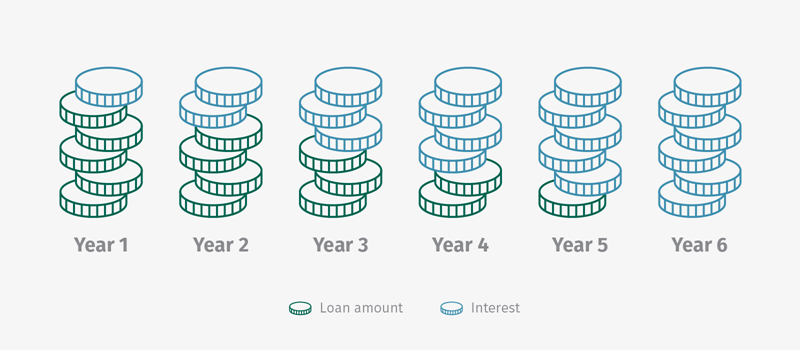

Refinancing

Student Loan Refinancing 101

Payment-saving Options

Home

Student Debt Counseling

Federal Student Loans

Ready, Get Set, Refinance

Refinancing

Student Loan Refinancing 101

Payment-saving Options

I need help from a pro

Explore Refinancing: find out what your friends already know

Explore Refinancing: find out what your friends already know

The benefits of paying off your student loans

01

Paves the way to reach other financial goals

02

Allows you to build up your savings

03

Helps with cash flow

04

Helps you handle other debt

05

Looks good on your credit history

The upside of clearing your student debt

- Financial freedom—plan, save, splurge.

- Less stress—financial, emotional, and physical.

- More free time—say no to that second job.

- Power to give generously—help those who helped you.

The Benefits of Paying Off Your Student Loans

1

Paves the way to reach other financial goals

Your debt-to-income (DTI) ratio is a sign of your financial fitness. Lower is better. A low DTI sends a signal to lenders that you’re able to responsibly borrow, such as for a mortgage. By paying off your student loan, you lower your DTI.

Paves the way to reach other financial goals

2

Allows you to build up your savings

Once you’ve paid off your loans, you’re free to turn those previous monthly payments into savings. You could save the same amount or a portion of it to build up an emergency fund or boost your nest egg.

Allows you to build up your savings

3

Helps with cash flow

Helps with cash flow

Without those monthly payments, you’ll have more money available for expenses. Or you may want to reward yourself for paying off your student debt. Does a vacation sound good?

Helps with cash flow

Helps with cash flow

4

Helps you handle other debt

Helps you handle other debt

If you have other high interest debt, you may want to focus on paying it down with the money you’re no longer using for student loans.

Helps you handle other debt

Helps you handle other debt

5

Looks good on your credit history

The credit bureaus know your payment history. When you’re on time, you’re looking good. Once you’ve made that final payment, however, you may see a dip in your credit score. It has to do with how credit scores are calculated. Don’t worry, though. Any drop is usually temporary.

Looks good on your credit history

Average Savings

$0

Average yearly customer savings†

Advice from the Experts

Refinancing terms to know

APR

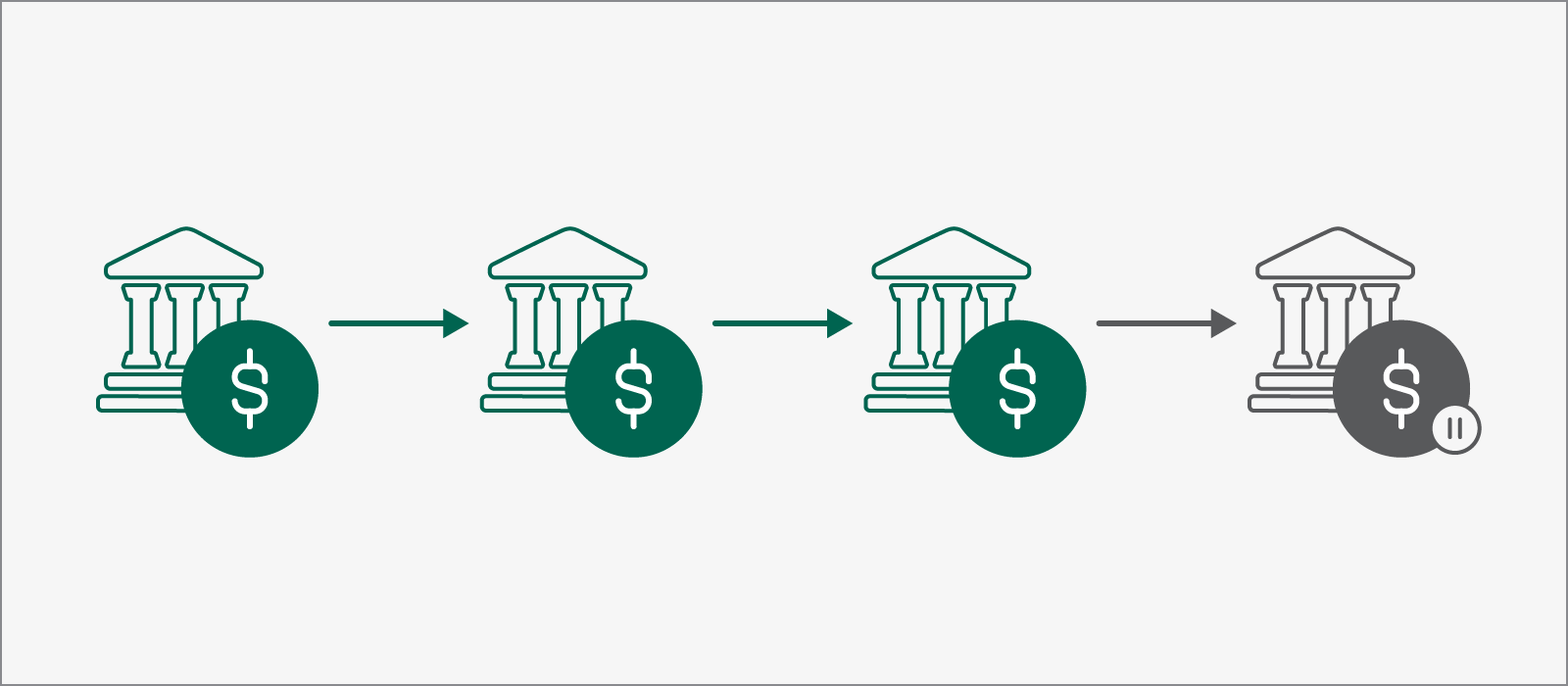

Consolidation

Deferment

Federal Forbearance

Fixed rate

Refinancing

Variable rate

Additional resources

Student Loan Refinancing: What Are the Benefits?

Average Student Loan Debt Statistics

What’s Student Loan Deferment vs. Forbearance?

Fast track to financial freedom

It’s never too late to save. Get started and you could save on average $352† monthly when you refinance your student loans into one easy payment.

Home

Home

Benefits of Paying

Off Student Loans

Benefits of Paying

Off Student Loans

Average

Savings

Average

Savings

Glossary

Glossary

I need help from a pro